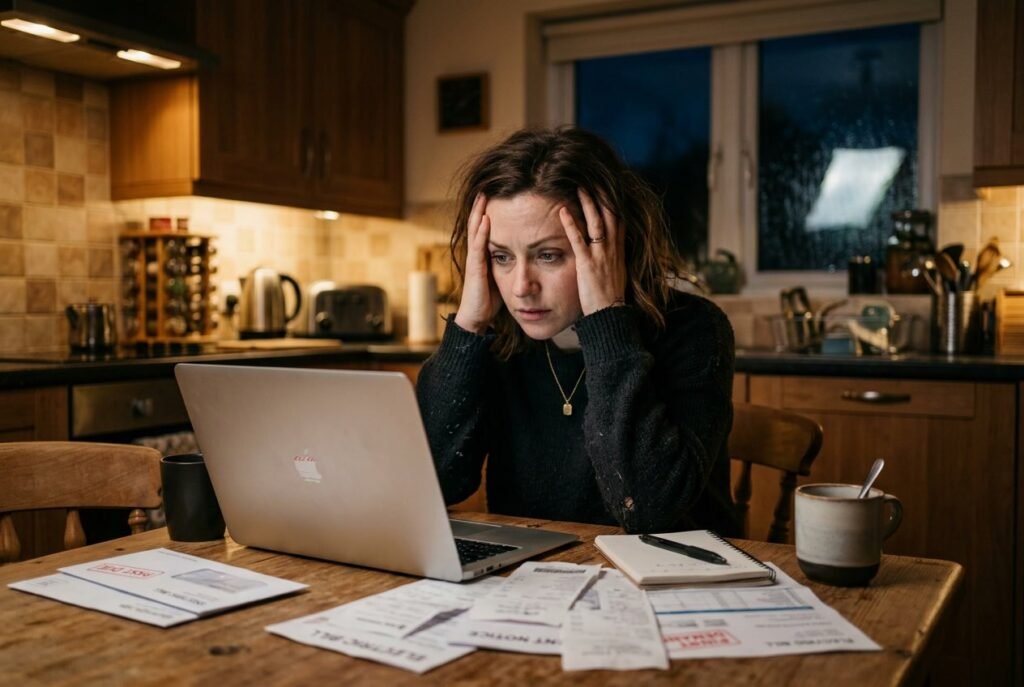

Most people think a steady job with regular paychecks means financial security. But relying on a single paycheck is one of the biggest financial risks you can take in today’s economy.

When that single paycheck stops, whether from layoffs, health issues, or company downsizing, your entire financial life can fall apart in weeks.

Job security isn’t what it used to be. Companies cut workers without warning. Costs keep climbing while wages stay flat. Your reliable income today could vanish tomorrow, and most people have no backup plan.

The good news is you don’t have to stay trapped.

This article breaks down why depending on one paycheck puts you at risk and shows you real ways to build multiple streams of income that protect your future.

You’ll learn the same strategies wealthy people use to create financial breathing room, even if you’re starting from scratch.

The Harsh Reality of Relying on a Single Paycheck

When your entire financial life depends on one income stream, you’re gambling with your stability.

Job loss can strike without warning, wages barely keep pace with inflation, and what seems like secure employment today can vanish tomorrow.

Job Loss and Financial Risk

Your job can disappear faster than you think. Companies downsize, industries collapse, and positions get eliminated regardless of how well you perform.

When you rely on a single paycheck, losing that job means your income drops to zero immediately.

Most people don’t have enough savings to handle this reality. Living paycheck to paycheck affects millions of Americans, leaving no buffer when unemployment hits.

Your bills don’t stop coming. Your mortgage, car payment, insurance, and groceries still need to be paid.

Without backup income sources, you’re forced into uncomfortable choices fast. You might drain retirement accounts, rack up credit card debt, or skip essential expenses.

The financial damage from a single job loss can take years to recover from, especially if you were already living close to the edge.

Stagnant Wages Versus Rising Living Costs

Your paycheck probably hasn’t grown much in recent years. Meanwhile, everything costs more.

Gas, groceries, rent, healthcare, and utilities all climb higher while your salary crawls forward at a fraction of that pace.

Inflation drives up prices faster than wages increase, creating a squeeze that gets tighter each year. A salary that felt comfortable five years ago barely covers basics now.

You’re working the same hours but falling further behind financially.

This gap creates real problems. You cut back on necessities, delay important purchases, and watch your quality of life decline.

When one income can’t keep up with rising costs, you have no margin for error and no room to save for the future.

The Illusion of Job Security

You might think your job is safe, but that security is mostly in your head. No position is guaranteed, no matter how long you’ve been there or how essential you feel.

Layoffs, company closures, and economic downturns eliminate jobs without warning.

Even profitable companies cut staff when they want to boost earnings. Mergers eliminate redundant positions. Technology replaces workers.

Management changes bring new priorities that don’t include you.

Your decades of loyalty mean nothing when the decision comes down. The false sense of security keeps you from building other income sources until it’s too late.

By the time you realize your job wasn’t as stable as you thought, you’re already unemployed and scrambling.

The One Point of Failure Problem

Your entire financial system collapses if one thing goes wrong. That’s what happens when everything depends on a single income source.

One illness, one accident, one company decision, and your whole life gets derailed.

This setup offers zero redundancy. Engineers would never design critical systems this way because they understand that single points of failure guarantee eventual catastrophe.

Economic downturns impact entire industries, meaning your vulnerability extends beyond just your specific employer.

The smart approach involves diversification. Multiple income streams mean losing one doesn’t destroy everything.

But most people never build that protection because their single paycheck keeps them too busy surviving to plan ahead.

Why It’s a Trap: The True Risks of Depending on One Income

When you live on one paycheck, you’re walking a tightrope with no net. Emergency costs hit without warning, prices climb faster than your salary, and one bad month can push you straight into debt.

Unpredictable Emergencies That Ruin Plans

Your car breaks down. Your kid needs urgent dental work. The water heater dies on a Sunday night.

These aren’t hypothetical scenarios. They’re the financial dangers that hit single-income families the hardest because there’s no backup cash flow.

Most experts tell you to keep three to six months of expenses in an emergency fund, but when you’re stretched thin on one income, building that cushion feels impossible.

Without a financial safety net, you face two bad choices. You can drain whatever savings you have, leaving yourself exposed to the next crisis.

Or you take on credit card debt at 20% interest that compounds every month you can’t pay it off in full.

The brutal truth is that one unexpected $2,000 expense can derail years of careful budgeting.

Your emergency fund gets wiped out, and you’re back to living paycheck to paycheck, except now you’re also trying to pay off debt on top of regular bills.

Inflation Chokes Your Earning Power

Your rent goes up $150 this year. Groceries cost 30% more than they did three years ago. Gas prices swing wildly, but they never seem to drop back to where they were.

Inflation eats away at your purchasing power while your single paycheck stays mostly flat.

Even if you get a 3% annual raise, that doesn’t mean much when everyday costs climb 5% to 8% in the same period.

You’re actually making less money in real terms.

This squeeze gets tighter every year. You start cutting back on things that used to be normal: eating out less, skipping vacations, putting off car maintenance.

The lifestyle you could afford five years ago slowly slips away, and your income hasn’t technically changed at all.

No Backup Means Faster Debt Traps

When your only income source can’t cover your monthly bills, the math gets simple and ugly. You charge essentials to credit cards. You take out personal loans. You borrow from family.

The problem compounds because debt payments become another fixed expense fighting for space in your already-tight budget.

Now you’re not just struggling to cover rent and groceries. You’re also sending $200, $500, or $800 every month to credit card companies and lenders.

This creates a vicious cycle. The more you rely on debt to fill gaps, the less money you have for actual expenses.

So you borrow more. The minimum payments climb higher.

Your credit score drops, which means higher interest rates on future loans.

One income can’t keep up with this spiral, and depending on a single paycheck leaves you with nowhere to turn when the walls close in.

How the Wealthy Escape: Building Multiple Income Streams

Wealthy people don’t wait around hoping their job stays secure. They create backup plans through diversified income sources that keep money flowing even when one stream dries up.

Passive Income Isn’t Just for the Rich

You don’t need a million dollars to start earning passive income. Dividend stocks let you collect checks just for owning shares.

A $500 monthly investment at 7% returns grows to $200,000 in 20 years.

Real estate rentals generate monthly cash without you clocking in. You can start small with a single rental property or invest in REITs if you can’t buy physical property yet.

Digital products work while you sleep. Create an online course once and sell it repeatedly. Write an ebook and earn royalties for years.

One tech millionaire studied earned $10,000 monthly from a blog on top of his salary.

The IRS reports that high-income households earn 30% of their money from investments, not wages.

Side Hustles: Your Lifeline

Your side hustle is your escape route from the single-paycheck trap. Freelancing generated $1.3 trillion in 2022, with 36% of Americans getting paid for extra work.

Start with skills you already have. Can you write? Code? Design? Teach? List three things you know how to do and figure out who will pay for them.

Sara Blakely built Spanx while keeping her day job. She didn’t quit until her side business proved itself.

Give it five hours weekly. That’s less than one hour per day. Research shows 51% of millionaires started with low-risk ventures they could manage alongside their main work.

Your side hustle becomes your safety net when your employer decides to cut costs.

Investing for Consistent Cash Flow

Investing builds wealth faster than saving alone. Put your money where it makes more money for you.

Smart investment options for steady income:

- Dividend stocks – Companies pay you quarterly just for holding shares

- Index funds – Spread risk across hundreds of companies automatically

- Bonds – Lower returns but more predictable payments

- ETFs – Trade like stocks but diversify your risk

Don’t dump everything into one investment. Wealthy people put no more than 10% of their income into new ventures according to financial planning research.

They spread money across different assets so one failure doesn’t wipe them out.

Build wealth through multiple income streams, not lottery thinking. Creating diversified earnings gives you the financial security that one paycheck never will.

Modern Ways to Diversify: Practical Steps Anyone Can Take

You don’t need a trust fund or MBA to build multiple income streams. Start with what you already know, pick one or two methods that match your skills, and build from there without burning out.

Freelancing and Consulting

Your current job skills are worth money outside your 9-to-5. Companies pay $50 to $200 per hour for specialized knowledge in marketing, design, accounting, or project management.

Start by identifying which income streams match your expertise. Pick one skill you use daily at work and offer it as a side hustle.

A marketing employee can run ad campaigns for small businesses. An accountant can do bookkeeping for local shops.

Getting your first clients:

- Post on LinkedIn about your availability

- Join industry-specific Facebook groups

- Message former colleagues who left for smaller companies

- List services on Upwork or Fiverr to build reviews

Set your rates higher than you think. Most freelancers undercharge at first and regret it. If someone balks at $75 per hour, they weren’t your client anyway.

Creating Digital Products

Digital products let you sell the same thing repeatedly without making it again.

Templates, guides, printables, and spreadsheets cost nothing to reproduce after you make them once.

Look at what you create for your own work or life. Budget spreadsheets, meal plans, resume templates, social media calendars.

Someone else needs what you already built.

Etsy sellers make steady money from simple products like wedding invitation templates or business card designs. You create it once, list it, and earn while you sleep.

Best digital products to start:

- Templates (Canva, Excel, Google Sheets)

- Printable planners or worksheets

- Checklists and how-to guides

- Stock photos or graphics

Price low at first ($5-$15) to get reviews and sales data. You can raise prices once you prove people want it.

Affiliate Marketing and Online Courses

Affiliate marketing pays you commissions for recommending products you already use. Sign up for Amazon Associates, ShareASale, or company-specific programs.

Don’t promote garbage just for commissions. Recommend what you actually bought and like. Your credibility matters more than a quick $20.

Online courses take more work upfront but can generate consistent monthly income once launched.

Start small with a $50 mini-course teaching one specific skill. Test if people will pay before building a massive program.

Record videos on your phone. Edit in free software. Host on Teachable or Gumroad. You don’t need fancy equipment to start.

Real Estate Moves and REITs

Rental properties build wealth but require serious cash upfront. Most mortgages need 20-25% down for investment properties. A $200,000 rental means bringing $40,000 to closing.

Can’t afford that? REITs (Real Estate Investment Trusts) let you invest in real estate with as little as $100.

You buy shares like stocks and earn dividend payments from rent collected on commercial properties, apartments, or warehouses.

REIT vs Physical Property:

| REITs | Rental Property |

|---|---|

| Start with $100 | Need $30,000+ down payment |

| No maintenance calls | Handle tenant issues |

| Sell anytime | Takes months to sell |

| Lower returns (3-5%) | Higher returns (8-12%) |

Dividend stocks from REITs pay quarterly. Vanguard Real Estate ETF (VNQ) and Schwab U.S. REIT ETF give you exposure to hundreds of properties without being a landlord.

Physical rentals work if you can handle 2 AM plumbing emergencies and tenant turnover. House hacking cuts your entry cost—buy a duplex, live in one unit, rent the other to cover your mortgage.

Skills and Mindset: Building Your Own Safety Net

Your job can disappear overnight, but the skills you build stay with you forever. Learning how to market yourself and turn side work into steady income creates real protection when a single paycheck fails.

Why In-Demand Skills Matter More Than Ever

The company doesn’t care about your loyalty when budget cuts come. You need skills that other employers actually want to pay for.

Tech skills like coding, data analysis, and digital marketing top the list right now. But don’t overlook trades like plumbing, electrical work, or HVAC repair.

These jobs can’t be outsourced to another country.

Focus on skills with clear market demand. Check job boards to see what employers are actively hiring for. Look at salary ranges to find which skills pay the most.

High-value skills worth learning:

- Web development – businesses always need websites

- Copywriting – companies need sales pages and emails

- Video editing – content creation isn’t slowing down

- Project management – every industry needs organized people

- Financial analysis – data-driven decisions rule business

You don’t need a four-year degree for most of these. Online courses, YouTube tutorials, and practice projects can get you hired.

Mastering the Art of Marketing Yourself

Nobody will hire you for skills they don’t know you have. You need to get loud about what you can do.

Start with LinkedIn. Write a profile that lists specific results, not vague descriptions. “Increased email open rates by 34%” beats “good at email marketing” every time.

Build a portfolio that shows real work. Create sample projects if you don’t have client work yet. A designer needs visual examples. A writer needs published articles or samples.

Network with people in your target field. Join online communities, comment on posts, and offer helpful advice. Most opportunities come from connections, not cold applications.

Apply the same marketing strategies to yourself that businesses use to sell products. You’re selling your time and expertise.

Turning Side Income Into Lasting Security

Side income only matters if it actually shows up when you need it. Random gigs won’t save you when your main job disappears.

Pick one or two income streams and build them properly. Spreading yourself across ten different hustles means none of them work well. Focus creates results.

Start small but start now. Building multiple income streams takes time, and waiting until you lose your job is too late.

Track every dollar your side work brings in. Know which activities actually make money versus which ones just keep you busy. Cut the time-wasters.

Automate what you can. Digital products, rental income, and dividend stocks work while you sleep. Trade your time for money at first, then build systems that run without you.

Steps to make side income reliable:

- Choose income streams that match your skills

- Set specific monthly earnings goals

- Dedicate consistent hours each week

- Reinvest profits to grow faster

- Build client relationships that repeat

Your side income becomes your safety net when it covers your basic expenses. That’s when a single paycheck stops controlling your life.

Preparation, Not Panic: Protecting Your Future

Building financial defenses means putting money aside for emergencies and securing your retirement through smart investing decisions. These two actions create a buffer between you and financial disaster.

Planning for Setbacks Before They Happen

You need cash on hand when things go wrong. An emergency fund isn’t optional when you’re living on one income.

Start with $1,000 in a savings account. This covers most small emergencies like car repairs or urgent medical bills. Then work toward three to six months of expenses.

How to build your emergency fund:

- Set up automatic transfers to savings each payday

- Save tax refunds and work bonuses

- Cut one non-essential expense and redirect that money

- Sell items you don’t use anymore

Keep this money in a high-yield savings account where you can access it quickly. Don’t invest your emergency fund in stocks or anything that could lose value when you need it most.

The reality is simple. 62% of Americans were living paycheck to paycheck in 2023. Without savings, one bad week destroys everything you’ve built.

401k and Long-Term Security Moves

Your 401k is your best tool for retirement if your employer offers one. The money goes in before taxes, which means you pay less to the IRS right now.

Maximize your 401k benefits:

- Contribute enough to get the full employer match

- Increase contributions by 1% every year

- Choose low-cost index funds over actively managed funds

- Never cash out early unless you face actual homelessness

If your company matches 3% of your salary, you’re throwing away free money by not contributing at least that much. That’s a guaranteed 100% return on your investment.

Beyond your 401k, consider opening a Roth IRA if you qualify. You pay taxes on this money now, but it grows tax-free forever. You can contribute up to $7,000 per year in 2026 if you’re under 50.

Start wherever you are. Even $50 per month invested consistently for 30 years becomes real money.

Final Thoughts

Relying on a single paycheck is dangerous. That sense of “safety” is a trap. You’re one corporate restructure or medical emergency away from total collapse.

Real security isn’t a salary; it’s the leverage that comes from having options when things go wrong.

The grind to diversify is brutal and slow. It requires sacrificing your free time to build systems that actually pay you. But the alternative is far worse: spending your life praying a boss you barely know decides to keep paying your bills.

Stop kidding yourself that there’s a perfect time to start.

Build your leverage now, or stay one bad Tuesday away from losing everything. Your future depends on the moves you make today.